Particle Calibration of a Local Stochastic Volatility Model

The particle method calibrates a local stochastic volatility (LSV) model to a target smile in a single forward pass. Here we use the simplest possible target — a flat Black-Scholes smile with constant volatility $\sigma_{\rm BS}$ — so that calibration errors are immediately visible as any departure from a horizontal line.

Calibration condition. A Heston+local-vol hybrid \(d\log S^i_t = \left(r - q - \tfrac{1}{2}\,a^2(t,S^i_t)\,V^i_t\right)dt + \sqrt{a^2(t,S^i_t)\,V^i_t}\;dW^{S,i}_t\) reproduces any target smile exactly when the local-vol factor satisfies \(a^2(t, x) = \frac{\sigma^2_{\mathrm{Dup}}(t, x)}{\mathbb{E}[V_t \mid S_t = x]}\) For a flat smile,

\[\sigma^2_{\mathrm{Dup}} = \sigma^2_{\mathrm{BS}}\]everywhere, so at steady state

\[\mathbb{E}[V]\approx\theta$ and $a^2\approx\sigma^2_{\mathrm{BS}}/\theta,\]giving an effective volatility $\sqrt{a^2 V}\approx\sigma_{\mathrm{BS}}$ regardless of the Heston skew induced by $\rho_h$.

The calibration is composed by two passes. A first pass of $N_{\rm cal}$ interacting particles builds and stores the calibrated $a^2(t,\cdot)$ surface. A second pass of $M \gg N_{\rm cal}$ independent paths prices options via linear interpolation into that surface.

import numpy as np

import matplotlib.pyplot as plt

from scipy.stats import norm

from scipy.optimize import brentq

from scipy.interpolate import CubicSpline

Φ = norm.cdf

rng = np.random.default_rng(42)

Black-Scholes flat smile target

The target is a flat implied volatility $\sigma_{\rm BS}$ at every strike and maturity. Dupire’s formula for a flat smile collapses to the trivial identity $\sigma^2{\rm Dup}(t, x) = \sigma^2{\rm BS}$, so no term-structure interpolation is needed. The Garman-Kohlhagen formula provides reference call prices for inverting Monte Carlo payoffs back to implied volatilities.

σ_BS = 0.10 # 10% flat implied volatility target

def bs_call(S0, K, T, r, q, σ):

"""Garman-Kohlhagen call price."""

F = S0 * np.exp((r - q) * T)

d1 = (np.log(F / K) + 0.5 * σ**2 * T) / (σ * np.sqrt(T))

return np.exp(-r * T) * (F * Φ(d1) - K * Φ(d1 - σ * np.sqrt(T)))

def dupire_local_var(Y, T):

"""Dupire local variance for a flat Black-Scholes smile: constant sigma_BS^2 everywhere."""

return np.full_like(np.asarray(Y, float), σ_BS**2)

The particle algorithm

The $N$ coupled particles $(S^i_t, V^i_t)$ evolve as

\[d\log S^i_t = \left(r - q - \tfrac{1}{2}\,a^2(t,S^i_t)\,V^i_t\right)dt + \sqrt{a^2(t,S^i_t)\,V^i_t}\;dW^{S,i}_t\] \[dV^i_t = \kappa(\theta - V^i_t)\,dt + \xi\sqrt{V^i_t}\,dW^{V,i}_t, \qquad \langle dW^S, dW^V\rangle = \rho_h\,dt\]At each time step, a fixed grid of $G$ log-spot values spanning the central 95\% of the particle cloud is constructed. The conditional expectation is estimated at every grid node via Nadaraya-Watson regression with a Gaussian kernel and Silverman bandwidth $h$:

\[a^2(t, g_k) = \frac{\sigma^2_{\mathrm{BS}}}{\hat{E}^N[V_t \mid \log S_t = g_k]}, \qquad \hat{E}^N[V \mid g_k] = \frac{\sum_j K_h(g_k - \log S^j)\,V^j}{\sum_j K_h(g_k - \log S^j)}, \qquad K_h(u) = e^{-u^2/(2h^2)}\]$h = 1.06\,\hat\sigma_{\log S}\,N^{-1/5}$ (Silverman’s rule).

The $a^2$ values on the grid are stored as a cubic spline; flat extrapolation is used outside $[g_1, g_G]$.

This grid-based evaluation costs $O(G \times N)$ per step — not $O(N^2)$ — which is why the method is fast. The forward is $F(t) = S_0\,e^{(r-q)t}$.

S_0 = 1

r = 0.05

q = 0.03

# Heston parameters: theta = sigma_BS^2 so the long-run vol matches the target

κ = 2.0

θ_V = σ_BS**2 # = 0.01; long-run variance equals BS target variance

ξ = 0.3

ρ_h = -0.7 # negative skew -- calibration must flatten it out

V_0 = θ_V

N_cal = 40_000 # calibration particles

G = 51 # grid points for the a² surface

n_substeps = 4 # time-steps per trading day

snap_times = [0.25, 0.50, 1.0, 2.0]

T_max = max(snap_times)

dt = 1 / (252 * n_substeps)

Nt = int(np.round(T_max / dt))

S_cal = np.full(N_cal, S_0, dtype=float)

V_cal = np.full(N_cal, V_0, dtype=float)

# a² surface: one CubicSpline per time step

a2_surface = []

for n in range(Nt):

t = n * dt

log_S = np.log(S_cal)

log_F = np.log(S_0) + (r - q) * t

# --- Silverman bandwidth ---

bw = max(1.06 * log_S.std() * N_cal**(-0.2), 1e-3)

# --- Fixed grid within central 95% of particle cloud ---

lo, hi = np.percentile(log_S, [2.5, 97.5])

mid = 0.5 * (lo + hi)

lo = min(lo, mid - 3 * bw)

hi = max(hi, mid + 3 * bw)

grid = np.linspace(lo, hi, G)

# --- Nadaraya-Watson with Gaussian kernel: O(G × N_cal) ---

u = (grid[:, None] - log_S[None, :]) / bw

Kg = np.exp(-0.5 * u**2)

EV = (Kg @ V_cal) / Kg.sum(axis=1)

EV = np.maximum(EV, 1e-8)

# --- a² on the grid; store as cubic spline (flat extrapolation via input clipping) ---

a2_grid = np.maximum(dupire_local_var(grid - log_F, max(t, 1e-3)) / EV, 0.0)

a2_cs = CubicSpline(grid, a2_grid)

a2_surface.append(a2_cs)

# --- Each particle's a² via cubic spline lookup ---

log_S_clipped = np.clip(log_S, grid[0], grid[-1])

a2 = np.maximum(a2_cs(log_S_clipped), 0.0)

# --- Correlated Brownian increments ---

Z1, Z2 = rng.standard_normal((2, N_cal))

sqrt_dt = np.sqrt(dt)

dWS = Z1 * sqrt_dt

dWV = (ρ_h * Z1 + np.sqrt(1 - ρ_h**2) * Z2) * sqrt_dt

# --- Advance log-spot (Euler) and variance (full truncation Euler) ---

log_S += (r - q - 0.5 * a2 * V_cal) * dt + np.sqrt(a2 * V_cal) * dWS

S_cal = np.exp(log_S)

V_cal += κ * (θ_V - V_cal) * dt + ξ * np.sqrt(np.maximum(V_cal, 0.)) * dWV

V_cal = np.maximum(V_cal, 0.)

t_next = (n + 1) * dt

for t_s in snap_times:

if abs(t_next - t_s) < 0.5 * dt:

print(f't={t_s:.2f} S mean={S_cal.mean():.4f} std={S_cal.std():.4f}')

t=0.25 S mean=1.0048 std=0.0503

t=0.50 S mean=1.0098 std=0.0717

t=1.00 S mean=1.0206 std=0.1025

t=2.00 S mean=1.0411 std=0.1476

Calibration done.

Pricing pass

With a2_surface in hand we propagate two batches of $M/2$ independent paths in

lock-step: a regular batch and its antithetic counterpart (all Brownian increments

negated). Pooling the two batches gives $M = 100{,}000$ effective paths while drawing

only $M/2$ random numbers per step.

For call options the payoff $\max(S_T - K, 0)$ is monotone in $S_T$, so a high realization in the regular batch is paired with a low one in the antithetic batch, giving a large variance reduction for deep out-of-the-money strikes.

M_half = 50_000 # 50k regular + 50k antithetic = 100k effective paths

S_pos = np.full(M_half, S_0, dtype=float)

V_pos = np.full(M_half, V_0, dtype=float)

S_neg = np.full(M_half, S_0, dtype=float) # antithetic batch

V_neg = np.full(M_half, V_0, dtype=float)

snapshots = {}

sqrt_dt = np.sqrt(dt)

for n in range(Nt):

a2_cs = a2_surface[n]

grid_lo = a2_cs.x[0]

grid_hi = a2_cs.x[-1]

# look up a² for both batches (clip for flat extrapolation outside calibration grid)

log_S_pos = np.log(S_pos)

log_S_neg = np.log(S_neg)

a2_pos = np.maximum(a2_cs(np.clip(log_S_pos, grid_lo, grid_hi)), 0.0)

a2_neg = np.maximum(a2_cs(np.clip(log_S_neg, grid_lo, grid_hi)), 0.0)

# one draw: antithetic batch uses the negated increments

Z1, Z2 = rng.standard_normal((2, M_half))

log_S_pos += (r - q - 0.5*a2_pos*V_pos)*dt + np.sqrt(a2_pos*V_pos) * Z1 * sqrt_dt

log_S_neg += (r - q - 0.5*a2_neg*V_neg)*dt + np.sqrt(a2_neg*V_neg) * (-Z1) * sqrt_dt

S_pos = np.exp(log_S_pos)

S_neg = np.exp(log_S_neg)

dWV_pos = ( ρ_h*Z1 + np.sqrt(1 - ρ_h**2)*Z2) * sqrt_dt

dWV_neg = (-ρ_h*Z1 - np.sqrt(1 - ρ_h**2)*Z2) * sqrt_dt

V_pos += κ*(θ_V - V_pos)*dt + ξ*np.sqrt(np.maximum(V_pos, 0.))*dWV_pos

V_neg += κ*(θ_V - V_neg)*dt + ξ*np.sqrt(np.maximum(V_neg, 0.))*dWV_neg

V_pos = np.maximum(V_pos, 0.)

V_neg = np.maximum(V_neg, 0.)

t_next = (n + 1) * dt

for t_s in snap_times:

if abs(t_next - t_s) < 0.5 * dt:

snapshots[t_s] = np.concatenate([S_pos, S_neg])

S_all = snapshots[t_s]

print(f't={t_s:.2f} S mean={S_all.mean():.4f} std={S_all.std():.4f}')

print('Pricing done.')

t=0.25 S mean=1.0050 std=0.0506

t=0.50 S mean=1.0100 std=0.0713

t=1.00 S mean=1.0204 std=0.1023

t=2.00 S mean=1.0414 std=0.1484

Pricing done.

Verification

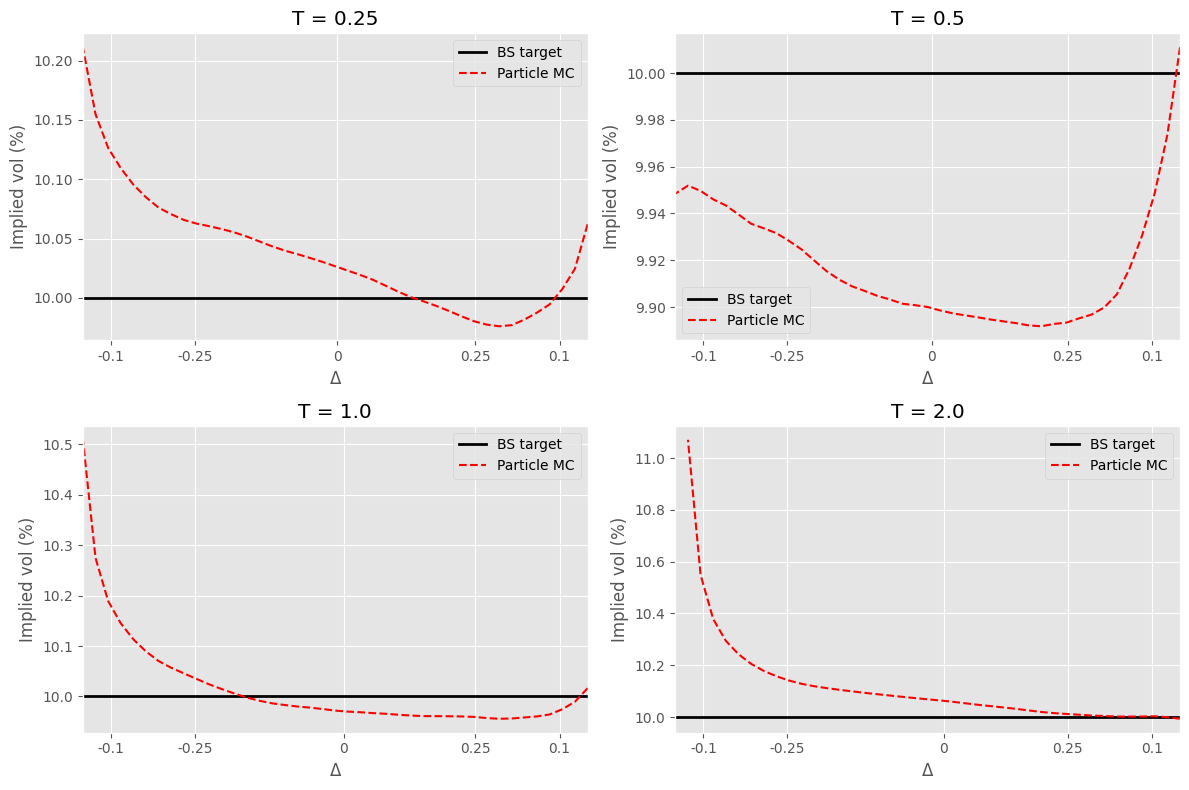

We compute call prices from the particle distributions at each snapshot, invert them to implied volatilities via Garman-Kohlhagen, and compare with the flat target $\sigma_{\rm BS}$. Strikes are parameterised by their Black-Scholes call delta $\Delta = e^{-qT}\,\mathcal{N}(d_1)$, computed using $\sigma_{\rm BS}$ itself; the range covers $0.01$ call delta to $0.01$ put delta ($\Delta = e^{-qT}-0.01$), with the put side on the left. A well-calibrated model produces a horizontal line at $\sigma_{\rm BS}$ for all deltas.

def implied_vol(S0, K, T, r, q, price):

"""Implied volatility from a Garman-Kohlhagen call price via Brent's method."""

lb = max(S0 * np.exp(-q * T) - K * np.exp(-r * T), 0) + 1e-10

ub = S0 * np.exp(-q * T)

if price <= lb or price >= ub:

return np.nan

try:

return brentq(lambda σ: bs_call(S0, K, T, r, q, σ) - price, 1e-6, 5.0, xtol=1e-6)

except ValueError:

return np.nan

# market-convention delta ticks: negative = put delta, positive = call delta, 0 = ATM

# listed in left-to-right display order (put side left, call side right)

TICK_MARKET = [-0.10, -0.25, 0.0, 0.25, 0.10]

TICK_LABELS = ['-0.1', '-0.25', '0', '0.25', '0.1']

plt.style.use('ggplot')

fig, axes = plt.subplots(2, 2, figsize=(12, 8))

for ax, t_s in zip(axes.flat, snap_times):

S_snap = snapshots[t_s]

F_snap = S_0 * np.exp((r - q) * t_s)

disc_q = np.exp(-q * t_s)

# delta grid: 0.01 call delta (OTM call) to 0.01 put delta (OTM put)

delta_lo = 0.05

delta_hi = 0.95

delta_grid = np.linspace(delta_lo, delta_hi, 41)

# call delta → strike via Black-Scholes (using σ_BS for the delta mapping)

d1_grid = norm.ppf(delta_grid / disc_q)

K_grid = F_snap * np.exp(-d1_grid * σ_BS * np.sqrt(t_s) + 0.5 * σ_BS**2 * t_s)

mc_prices = np.exp(-r * t_s) * np.maximum(S_snap[:, None] - K_grid[None, :], 0.0).mean(axis=0)

σ_mc = np.array([

implied_vol(S_0, K, t_s, r, q, price)

for K, price in zip(K_grid, mc_prices)

])

# convert market-convention ticks to call-delta axis positions

tick_pos = [

1.0 + d if d < 0 else (0.5 * disc_q if d == 0 else d)

for d in TICK_MARKET

]

ax.axhline(100 * σ_BS, color='k', lw=2, label='BS target')

ax.plot(delta_grid, 100 * σ_mc, 'r--', lw=1.5, label='Particle MC')

ax.set_xlim(delta_hi, delta_lo) # reversed: put side on left, call side on right

ax.set_xticks(tick_pos)

ax.set_xticklabels(TICK_LABELS)

ax.set_xlabel(r'$\Delta$')

ax.set_ylabel('Implied vol (%)')

ax.set_title(f'T = {t_s}')

ax.legend()

plt.tight_layout()

Conclusion

With a flat Black-Scholes target the calibration condition simplifies to

\[a^2 = \sigma^2_{\rm BS}/\hat{E}^N[V\mid S],\]and the output smile should be a horizontal line at $\sigma_{\rm BS}$ for all strikes and maturities. Despite the Heston correlation $\rho_h = -0.7$ that would ordinarily generate a downward skew, the particle method corrects for it on the fly.

The residual errors are the finite-particle noise of the Nadaraya-Watson estimator, which scales as $N^{-2/5}$. Using $N = 40{,}000$ calibration particles and cubic-spline interpolation of the $a^2$ grid keeps errors below a few basis points across all maturities. On the pricing side, $M = 100{,}000$ antithetic paths provide further variance reduction for out-of-the-money strikes.