This article is an extension of the previous one on the analysis of arXiv articles. While the scope is similar, it uses different language models and Python packages; the list of articles we consider is different as well.

We use a few specific packages:

- the arxiv package is used to download the articles metadata;

- the sentence transformers package is used for the embeddings;

- the faiss package is used for efficient similarity search and clustering of dense vectors;

- the KeyBERT is used for keyword extraction.

They can be installed (on CPU) using the following pip command:

pip install -U sentence-transformers faiss-cpu arxiv keybert

Our aim is to find the similarities of the latest articles in all the categories. We do this by downloading the metadata of the last 10,000 articles in each of the main categories and assembling them together. Once this is done, and after removing redundant entries, we compute an embedding for each article using its abstract, and proceed from there. This approach is a starting point: results could be improved with a model for the embedding stailored for scientific publications, like SciBERT; working with the full text as well the citations would improve the results substantially.

import arxiv

from itertools import count

from datetime import datetime

from IPython.display import display, HTML

import matplotlib.pylab as plt

import numpy as np

import pandas as pd

from pathlib import Path

import torch

from sentence_transformers import SentenceTransformer

import faiss

import pickle

def query(query, max_results=None, offset: int = 0):

search = arxiv.Search(

query=query,

max_results=max_results,

sort_by=arxiv.SortCriterion.LastUpdatedDate

)

client = arxiv.Client(num_retries=10, page_size=500)

return list(client.results(search=search, offset=offset))

cs = query('cat:cs.*', max_results=10_000)

econ = query('cat:econ.*', max_results=10_000)

eess = query('eess.*', max_results=10_000)

math = query('math.*', max_results=10_000)

qfin = query('q-fin.*', max_results=10_000)

stat = query('stat.*', max_results=10_000)

Since the calls to query() can be quite long, it is convenient to store the results in a pickle file for rerunning the notebook in the future.

with open('data.pickle', 'wb') as f:

pickle.dump((cs, econ, eess, math, qfin, stat), f)

with open('data.pickle', 'rb') as f:

cs, econ, eess, math, qfin, stat = pickle.load(f)

articles = cs + econ + eess + math + qfin + stat

Since some articles can be part of more than one search, we make sure there is only one reference to any title in our set.

from itertools import groupby

get_title = lambda x: x.title

articles = [next(v) for _, v in groupby(sorted(articles, key=get_title), get_title)]

print(f"# unique articles: {len(articles)}")

# unique articles: 49706

The [models](https://www.sbert.net/docs/pretrained_models.html we can choose from for computing the embeddings vary in complexity and computational cost. Overall they are all pretty slow and require a few gigabytes of memory; we choose all-MiniLM-L6-v2, which is ok for the scope of this article. This is a sentence-transformers model: It maps sentences and paragraphs to a 384 dimensional dense vector space and can be used for tasks like clustering or semantic search.

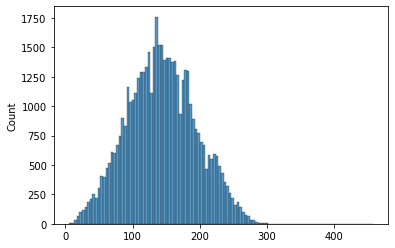

As reported in the model card, input text longer than 256 word pieces is truncated, so we must make sure that the text that is given in input is not too long. Plotting the histogram shows that we are mostly fine, with the vast majority of articles having less than 300 words. The distribution is quite symmetric, with a mean of about 145 words.

import seaborn as sns

sns.histplot(pd.Series([len(a.summary.split(' ')) for a in articles]))

<AxesSubplot:ylabel='Count'>

The code that calls the sequence transformer is very easy. Since it is time consuming, though, we save the results to a file.

from sentence_transformers import SentenceTransformer

model = SentenceTransformer('all-MiniLM-L6-v2')

embeddings = model.encode([a.summary for a in articles], show_progress_bar=True)

np.savez('embeddings.npz', embeddings)

At this point we need the faiss package. We use the $L_2$-norm for computing distances.

embeddings = np.load('embeddings.npz')['arr_0'].astype("float32")

index = faiss.IndexFlatL2(embeddings.shape[1])

index.add(embeddings)

As done in the previous article, we select the paper Variational Autoencoders: A Hands-Off Approach to Volatility and try to find similar ones.

for selected, article in enumerate(articles):

if article.title == 'Variational Autoencoders: A Hands-Off Approach to Volatility':

break

D, I = index.search(embeddings[selected:selected + 1], k=11)

html = '<table>'

for d, i in zip(D[0], I[0]):

if i == selected:

continue

article = articles[i]

pub_date = datetime.strftime(article.published, '%Y-%m-%d')

cat = article.primary_category

cats = ', '.join([cat] + [c for c in article.categories if c != cat])

link = article.links[0].href

html += f"<tr><td style=\"text-align:left\">distance: {d:.4f}, publication: {pub_date} [{cats}] <a href='{link}'>🔗</a><br>"

html += '<i>' + ', '.join((a.name for a in article.authors)) + "</i><br><b>" + article.title + "</b>"

html += "</td></tr>"

html += "</table>"

display(HTML(html))

| distance: 0.3913, publication: 2022-11-23 [q-fin.PR] 🔗 Zheng Gong, Wojciech Frys, Renzo Tiranti, Carmine Ventre, John O'Hara, Yingbo Bai A new encoding of implied volatility surfaces for their synthetic generation |

| distance: 0.5050, publication: 2022-08-30 [q-fin.CP] 🔗 Sándor Kunsági-Máté, Gábor Fáth, István Csabai, Gábor Molnár-Sáska Deep Weighted Monte Carlo: A hybrid option pricing framework using neural networks |

| distance: 0.5247, publication: 2021-08-10 [q-fin.MF, cs.LG, q-fin.CP, q-fin.PR, stat.ML] 🔗 Brian Ning, Sebastian Jaimungal, Xiaorong Zhang, Maxime Bergeron Arbitrage-Free Implied Volatility Surface Generation with Variational Autoencoders |

| distance: 0.5643, publication: 2023-03-01 [q-fin.CP, cs.LG, q-fin.ST, stat.ML, 91G60, 91G80, 62M45, 68T07] 🔗 Vedant Choudhary, Sebastian Jaimungal, Maxime Bergeron FuNVol: A Multi-Asset Implied Volatility Market Simulator using Functional Principal Components and Neural SDEs |

| distance: 0.6057, publication: 2020-05-05 [q-fin.CP, math.OC, stat.ML] 🔗 Christa Cuchiero, Wahid Khosrawi, Josef Teichmann A generative adversarial network approach to calibration of local stochastic volatility models |

| distance: 0.6196, publication: 2021-06-14 [q-fin.ST] 🔗 Wenyong Zhang, Lingfei Li, Gongqiu Zhang A Two-Step Framework for Arbitrage-Free Prediction of the Implied Volatility Surface |

| distance: 0.6638, publication: 2021-12-13 [q-fin.CP, cs.LG, q-fin.MF, q-fin.ST, stat.ML] 🔗 Magnus Wiese, Ben Wood, Alexandre Pachoud, Ralf Korn, Hans Buehler, Phillip Murray, Lianjun Bai Multi-Asset Spot and Option Market Simulation |

| distance: 0.7064, publication: 2021-12-09 [q-fin.CP, econ.EM] 🔗 Zhe Wang, Nicolas Privault, Claude Guet Deep self-consistent learning of local volatility |

| distance: 0.7308, publication: 2021-03-22 [q-fin.CP, cs.LG] 🔗 Jay Cao, Jacky Chen, John Hull, Zissis Poulos Deep Learning for Exotic Option Valuation |

| distance: 0.7525, publication: 2023-02-17 [q-fin.MF, q-fin.CP, 91G20, 91G60, 91G80, 47G10, 47G40, 35Q79,] 🔗 Alexander Lipton, Adil Reghai SPX, VIX and scale-invariant LSV\footnote{Local Stochastic Volatility} |

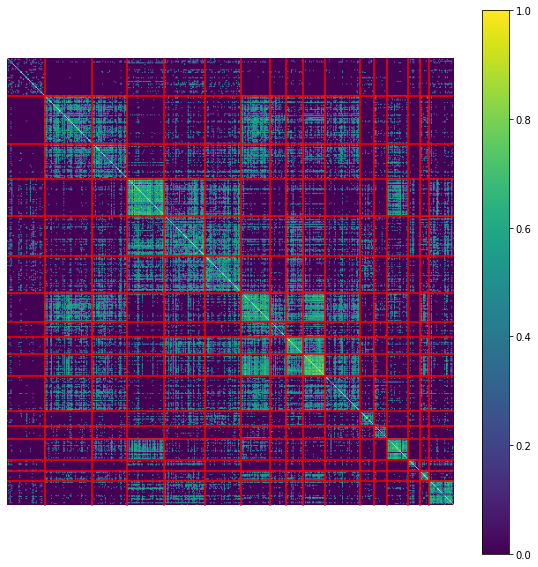

A more interesting approach is instead to look for clusters. Here we select all the articles that contain the work volatility in their title. On the date of execution we had 507 such articles; for this subset we use the agglomerative clustering algorithm provided by the scikit-learn library. After some experimentations, we use a distance threshold of 2.

sub_indices, sub_articles = [], []

for i, article in enumerate(articles):

if 'volatility' in article.title.lower():

sub_indices.append(i)

sub_articles.append(article)

print(f"Selected {len(sub_indices)} articles.")

E = embeddings[sub_indices]

num_articles = E.shape[0]

dist = (E @ E.T).round(1)

dist = np.where(dist < 0.5, 0.0, dist)

Selected 507 articles.

from sklearn.cluster import AgglomerativeClustering

from scipy.cluster.hierarchy import dendrogram, linkage

hierarchical_cluster = AgglomerativeClustering(n_clusters=None, distance_threshold=2,

metric='euclidean', linkage='ward')

labels = hierarchical_cluster.fit_predict(E)

We reorder our subset to have all the articles in the cluster #0 first, followed by the articles in cluster #1, and so on. Plotting the distance matrix using this new ordering shows a certain structure that was not visible in the original, unordered matrix. Clusters #3, #6, #9 and #16 are large are interconnected; clusters #8 and #13 smaller but quite distinct from the rest. Cluster #0 seems to be composed by articles that have little in common with the others, while cluster #1, #2, #4, #5 and #10 have weak connections.

perm = []

limits = []

for label in set(labels):

perm += pd.Series(labels)[labels == label].index.tolist()

limits.append(len(perm))

plt.figure(figsize=(10, 10))

plt.imshow(dist[perm, :][:, perm])

plt.colorbar()

plt.axis('equal')

plt.axis('off')

for limit in limits[:-1]:

plt.axhline(limit, xmin=0, xmax=1, color='red')

plt.axvline(limit, ymin=0.09, ymax=0.91, color='red')

What we do now is to print out a few articles for each cluster and a short list of keywords. For the latter we use KeyBert, which is relatively fast and free to use; the keywords are based on all the titles in each cluster.

from keybert import KeyBERT

kw_model = KeyBERT()

def get_articles(selected_label, max_entries):

retval = []

counter = 1

for label, article in zip(labels, reversed(sorted(sub_articles, key=lambda x: x.published))):

if label != selected_label: continue

retval.append(article)

counter += 1

if counter > max_entries: break

return retval

def get_keywords(articles):

text = []

for article in articles:

text.append(article.title)

text = '\n'.join(text)

keywords = kw_model.extract_keywords(text, keyphrase_ngram_range=(1, 2), stop_words=None)

return [k[0] for k in keywords]

def to_html(articles):

html = '<table>'

for article in articles:

pub_date = datetime.strftime(article.published, '%Y-%m-%d')

cat = article.primary_category

cats = ', '.join([cat] + [c for c in article.categories if c != cat])

link = article.links[0].href

html += f"<tr><td style=\"text-align:left\">published on {pub_date} [{cats}] <a href='{link}'>🔗</a><br>"

html += '<i>' + ', '.join((a.name for a in article.authors)) + "</i><br><b>" + article.title + "</b>"

html += "</td></tr>"

html += "</table>"

return html

for label in set(labels):

full_subset = get_articles(label, 1_000)

subset = get_articles(label, 5)

keywords = get_keywords(full_subset)

html = f'<p style="color: crimson;">Label #{label}, {len(full_subset)} articles'

html += f", keywords: {', '.join((k.title() for k in keywords))}"

html += to_html(subset)

display(HTML(html))

Label #0, 42 articles, keywords: Volatility Prediction, Volatility Predictions, Volatility Models, Financial Volatility, Volatility Evidence

| published on 2023-10-28 [cs.LG] 🔗 Shengkun Wang, YangXiao Bai, Kaiqun Fu, Linhan Wang, Chang-Tien Lu, Taoran Ji ALERTA-Net: A Temporal Distance-Aware Recurrent Networks for Stock Movement and Volatility Prediction |

| published on 2023-10-22 [econ.EM, stat.AP] 🔗 Joshua Chan BVARs and Stochastic Volatility |

| published on 2023-10-02 [q-fin.RM, cs.AI, cs.LG, q-fin.CP, q-fin.GN] 🔗 Jakub Michańków, Łukasz Kwiatkowski, Janusz Morajda Combining Deep Learning and GARCH Models for Financial Volatility and Risk Forecasting |

| published on 2023-09-14 [q-fin.CP, cs.AI, q-fin.MF, q-fin.PR, q-fin.RM] 🔗 Abir Sridi, Paul Bilokon Applying Deep Learning to Calibrate Stochastic Volatility Models |

| published on 2023-08-04 [q-fin.ST, cs.LG] 🔗 Damien Challet, Vincent Ragel Recurrent Neural Networks with more flexible memory: better predictions than rough volatility |

Label #1, 54 articles, keywords: Volatility Learning, Volatility Forecasting, Volatility Prediction, Forecasting Volatility, Volatility Estimation

| published on 2023-11-14 [math.PR, math.AP, q-fin.MF, 60G22, 35K10, 91G20] 🔗 Alexandre Pannier Path-dependent PDEs for volatility derivatives |

| published on 2023-10-26 [stat.AP, econ.EM] 🔗 Michele Costola, Matteo Iacopini, Casper Wichers Bayesian SAR model with stochastic volatility and multiple time-varying weights |

| published on 2023-10-23 [cs.CE, q-fin.ST] 🔗 Xin Du, Kai Moriyama, Kumiko Tanaka-Ishii Co-Training Realized Volatility Prediction Model with Neural Distributional Transformation |

| published on 2023-08-24 [econ.EM, q-fin.ST, stat.OT] 🔗 Philipp Otto, Osman Doğan, Süleyman Taşpınar, Wolfgang Schmid, Anil K. Bera Spatial and Spatiotemporal Volatility Models: A Review |

| published on 2023-07-25 [q-fin.TR, q-fin.PM] 🔗 Ivan Letteri VolTS: A Volatility-based Trading System to forecast Stock Markets Trend using Statistics and Machine Learning |

Label #2, 40 articles, keywords: Volatility Models, Volatility Smoothing, Volatility Pricing, Volatility Strategies, Volatility Forecasting

| published on 2023-10-25 [q-fin.CP] 🔗 Kentaro Hoshisashi, Carolyn E. Phelan, Paolo Barucca No-Arbitrage Deep Calibration for Volatility Smile and Skewness |

| published on 2022-12-21 [q-fin.MF, q-fin.CP] 🔗 Eduardo Abi Jaber, Camille Illand, Shaun, Li The quintic Ornstein-Uhlenbeck volatility model that jointly calibrates SPX & VIX smiles |

| published on 2022-12-20 [q-fin.MF, q-fin.CP, stat.ML] 🔗 Marc Chataigner, Areski Cousin, Stéphane Crépey, Matthew Dixon, Djibril Gueye Beyond Surrogate Modeling: Learning the Local Volatility Via Shape Constraints |

| published on 2022-12-16 [q-fin.MF, q-fin.CP] 🔗 Eduardo Abi Jaber, Camille Illand, Shaun, Li Joint SPX-VIX calibration with Gaussian polynomial volatility models: deep pricing with quantization hints |

| published on 2022-12-15 [q-fin.PR, math.PR, 60F10 (Primary) 91G20 (Secondary)] 🔗 Peter K. Friz, Thomas Wagenhofer Reconstructing Volatility: Pricing of Index Options under Rough Volatility |

Label #3, 42 articles, keywords: Stochastic Volatility, Volatility Models, Volatility Estimation, Hawkes Volatility, Hawkes Stochastic

| published on 2023-10-28 [math.PR, Primary 60H30, 60G44, secondary 60J60, 94A17] 🔗 Bertram Tschiderer Diffusion processes as Wasserstein gradient flows via stochastic control of the volatility matrix |

| published on 2023-09-30 [stat.ME] 🔗 Abdelbasset Djeniah, Mohamed Chaouch, Amina Angelika Bouchentouf Inference on volatility estimation with missing data: a functional data approach |

| published on 2023-09-26 [q-fin.MF, cs.NA, math.NA, 60H35, 68T07, 91G60] 🔗 Francesca Biagini, Lukas Gonon, Niklas Walter Approximation Rates for Deep Calibration of (Rough) Stochastic Volatility Models |

| published on 2023-07-18 [q-fin.MF, math.PR, 91G20, 91G60, 60L50] 🔗 Peter Bank, Christian Bayer, Peter K. Friz, Luca Pelizzari Rough PDEs for local stochastic volatility models |

| published on 2023-07-03 [econ.EM, stat.ME] 🔗 Ruijun Bu, Degui Li, Oliver Linton, Hanchao Wang Nonparametric Estimation of Large Spot Volatility Matrices for High-Frequency Financial Data |

Label #4, 46 articles, keywords: Volatility Forecasting, Predicting Volatility, Volatility Prediction, Learning Volatility, Volatility Modelling

| published on 2023-08-21 [cs.LG, cs.AI, stat.ML] 🔗 Pranay Pasula Real World Time Series Benchmark Datasets with Distribution Shifts: Global Crude Oil Price and Volatility |

| published on 2023-08-01 [q-fin.ST, cs.LG, q-fin.RM] 🔗 Chao Zhang, Xingyue Pu, Mihai Cucuringu, Xiaowen Dong Graph Neural Networks for Forecasting Multivariate Realized Volatility with Spillover Effects |

| published on 2023-07-18 [q-fin.RM, q-fin.ST] 🔗 Apostolos Ampountolas The Effect of COVID-19 on Cryptocurrencies and the Stock Market Volatility -- A Two-Stage DCC-EGARCH Model Analysis |

| published on 2023-06-26 [q-fin.MF, 91G20] 🔗 E. Alòs, F. Rolloos, K. Shiraya A lower bound for the volatility swap in the lognormal SABR model |

| published on 2023-06-20 [q-fin.ST, cs.LG, q-fin.CP, q-fin.RM] 🔗 Wenbo Ge, Pooia Lalbakhsh, Leigh Isai, Artem Lensky, Hanna Suominen Comparing Deep Learning Models for the Task of Volatility Prediction Using Multivariate Data |

Label #5, 41 articles, keywords: Volatility Forecasting, Volatility Prediction, Forecasting Volatility, Volatility Models, Volatility Modeling

| published on 2023-11-08 [q-fin.ST, q-fin.MF, q-fin.TR] 🔗 Siu Hin Tang, Mathieu Rosenbaum, Chao Zhou Forecasting Volatility with Machine Learning and Rough Volatility: Example from the Crypto-Winter |

| published on 2023-08-29 [q-fin.MF] 🔗 Elisa Alòs, Eulalia Nualart, Makar Pravosud On the implied volatility of European and Asian call options under the stochastic volatility Bachelier model |

| published on 2023-06-15 [econ.EM] 🔗 Andrea Renzetti Modelling and Forecasting Macroeconomic Risk with Time Varying Skewness Stochastic Volatility Models |

| published on 2023-06-05 [econ.EM] 🔗 Eiji Kurozumi, Anton Skrobotov Improving the accuracy of bubble date estimators under time-varying volatility |

| published on 2023-05-06 [stat.ME] 🔗 Piotr Kokoszka, Neda Mohammadi, Haonan Wang, Shixuan Wang Functional diffusion driven stochastic volatility model |

Label #6, 33 articles, keywords: Volatility Models, Volatility Forecasting, Volatility Processes, Volatility Estimation, Models Volatility

| published on 2023-09-07 [q-fin.PR, math.PR, 60G55, 60H30, 91G05, 91G15] 🔗 David R. Baños, Salvador Ortiz-Latorre, Oriol Zamora Font Thiele's PIDE for unit-linked policies in the Heston-Hawkes stochastic volatility model |

| published on 2023-08-02 [q-fin.CP] 🔗 Anoop C V, Neeraj Negi, Anup Aprem Bayesian framework for characterizing cryptocurrency market dynamics, structural dependency, and volatility using potential field |

| published on 2022-08-28 [econ.EM, stat.ME] 🔗 Joshua C. C. Chan Comparing Stochastic Volatility Specifications for Large Bayesian VARs |

| published on 2022-08-19 [econ.EM] 🔗 Avik Das, Dr. Devanjali Nandi Das Understanding Volatility Spillover Relationship Among G7 Nations And India During Covid-19 |

| published on 2022-07-21 [q-fin.MF, 91G99] 🔗 Elisa Alòs, Frido Rolloos, Kenichiro Shiraya Forward start volatility swaps in rough volatility models |

Label #7, 18 articles, keywords: Volatility Prediction, Volatility Forecasting, Volatility Modeling, Volatility Clustering, Rough Volatility

| published on 2023-09-02 [q-fin.MF, math.PR, 91-02, 91-03, 62P05, 60H10, 60G22, 91G15, 91G30, 91G80] 🔗 Giulia Di Nunno, Kęstutis Kubilius, Yuliya Mishura, Anton Yurchenko-Tytarenko From constant to rough: A survey of continuous volatility modeling |

| published on 2023-03-13 [q-fin.MF, q-fin.CP] 🔗 Eduardo Abi Jaber, Nathan De Carvalho Reconciling rough volatility with jumps |

| published on 2022-09-13 [q-fin.RM] 🔗 Aurélien Alfonsi, Nerea Vadillo A stochastic volatility model for the valuation of temperature derivatives |

| published on 2022-05-16 [econ.EM, stat.ML] 🔗 Rafael Reisenhofer, Xandro Bayer, Nikolaus Hautsch HARNet: A Convolutional Neural Network for Realized Volatility Forecasting |

| published on 2022-01-25 [q-fin.ST, q-fin.RM] 🔗 Giuseppe Brandi, T. Di Matteo Multiscaling and rough volatility: an empirical investigation |

Label #8, 19 articles, keywords: Rough Volatility, Volatility Models, Volatility Stochastic, Stochastic Volatility, Volatility Detecting

| published on 2023-07-05 [q-fin.ST, math.PR, math.ST, stat.TH] 🔗 Xiyue Han, Alexander Schied Estimating the roughness exponent of stochastic volatility from discrete observations of the realized variance |

| published on 2023-03-20 [stat.AP, econ.EM, q-fin.ST] 🔗 Raffaele Mattera, Philipp Otto Network log-ARCH models for forecasting stock market volatility |

| published on 2023-02-24 [q-fin.CP] 🔗 Camilla Damian, Rüdiger Frey Detecting Rough Volatility: A Filtering Approach |

| published on 2022-05-01 [q-fin.PR, Primary 91G20, Secondary 41A60, 44A99, 91G60] 🔗 Jiling Cao, Jeong-Hoon Kim, Xi Li, Wenjun Zhang Pricing Path-dependent Options under Stochastic Volatility via Mellin Transform |

| published on 2022-04-30 [q-fin.PR] 🔗 Frido Rolloos Hull and White and Alòs type formulas for barrier options in stochastic volatility models with nonzero correlation |

Label #9, 25 articles, keywords: Volatility Models, Volatility Identification, Volatility Dynamics, Volatility Forecasting, Volatility Estimation

| published on 2023-11-02 [q-fin.MF, math.PR, 91G30, 60H10, 60H35, 60G22] 🔗 Giulia Di Nunno, Anton Yurchenko-Tytarenko Power law in Sandwiched Volterra Volatility model |

| published on 2023-05-02 [econ.EM] 🔗 Sung Hoon Choi, Donggyu Kim Large Global Volatility Matrix Analysis Based on Observation Structural Information |

| published on 2023-03-16 [q-fin.ST] 🔗 Claudiu Vinte, Marcel Ausloos Portfolio Volatility Estimation Relative to Stock Market Cross-Sectional Intrinsic Entropy |

| published on 2022-07-08 [econ.EM, stat.ME] 🔗 Joshua Chan, Eric Eisenstat, Xuewen Yu Large Bayesian VARs with Factor Stochastic Volatility: Identification, Order Invariance and Structural Analysis |

| published on 2022-04-14 [q-fin.PR, econ.EM] 🔗 Peter Reinhard Hansen, Chen Tong Option Pricing with Time-Varying Volatility Risk Aversion |

Label #10, 40 articles, keywords: Volatility Forecasting, Volatility Estimation, Volatility Prediction, Volatility Models, Volatility Bayesian

| published on 2023-09-04 [q-fin.CP] 🔗 German Rodikov, Nino Antulov-Fantulin Introducing the $σ$-Cell: Unifying GARCH, Stochastic Fluctuations and Evolving Mechanisms in RNN-based Volatility Forecasting |

| published on 2023-08-30 [q-fin.PR] 🔗 Dan Pirjol, Lingjiong Zhu Asymptotics for Short Maturity Asian Options in a Jump-Diffusion model with Local Volatility |

| published on 2023-04-04 [q-fin.RM, cs.LG, q-fin.TR] 🔗 Mingyu Hao, Artem Lenskiy Short-Term Volatility Prediction Using Deep CNNs Trained on Order Flow |

| published on 2023-03-29 [q-fin.RM, q-fin.ST] 🔗 Ke Zhang Adjust factor with volatility model using MAXFLAT low-pass filter and construct portfolio in China A share market |

| published on 2023-03-29 [q-fin.MF, q-fin.GN] 🔗 Gurdip Bakshi, John Crosby, Xiaohui Gao Dark Matter in (Volatility and) Equity Option Risk Premiums |

Label #11, 16 articles, keywords: Volatility Models, Volatility Forecasting, Volatility Clustering, Volatility Estimation, Stochastic Volatility

| published on 2023-09-09 [q-fin.GN, econ.TH] 🔗 Sabiou Inoua News-driven Expectations and Volatility Clustering |

| published on 2023-07-03 [q-fin.PR, math.PR, 60H10, 91G20] 🔗 Marcel Nutz, Andrés Riveros Valdevenito On the Guyon-Lekeufack Volatility Model |

| published on 2023-03-27 [q-fin.ST] 🔗 Christoph J. Börner, Ingo Hoffmann, John H. Stiebel On the Connection between Temperature and Volatility in Ideal Agent Systems |

| published on 2022-11-28 [q-fin.MF, math.PR, 60G44, 60J60, 91G10 (Primary) 60J46 (Secondary)] 🔗 David Itkin, Benedikt Koch, Martin Larsson, Josef Teichmann Ergodic robust maximization of asymptotic growth under stochastic volatility |

| published on 2022-07-01 [q-fin.CP, q-fin.MF] 🔗 Weilong Fu, Ali Hirsa Solving barrier options under stochastic volatility using deep learning |

Label #12, 15 articles, keywords: Volatility Prediction, Volatility Models, Volatility Based, Volatility Selection, Stochastic Volatility

| published on 2023-09-28 [q-fin.ST] 🔗 Wenting Liu, Zhaozhong Gui, Guilin Jiang, Lihua Tang, Lichun Zhou, Wan Leng, Xulong Zhang, Yujiang Liu Stock Volatility Prediction Based on Transformer Model Using Mixed-Frequency Data |

| published on 2023-06-19 [q-fin.PM, 91G10, 49L20] 🔗 Marcos Escobar-Anel, Michel Kschonnek, Rudi Zagst Mind the Cap! -- Constrained Portfolio Optimisation in Heston's Stochastic Volatility Model |

| published on 2023-06-18 [econ.GN, q-fin.EC] 🔗 Ali Lashgari Harnessing the Potential of Volatility: Advancing GDP Prediction |

| published on 2022-06-05 [q-fin.GN, math.PR] 🔗 R. Vilela Mendes The fractional volatility model and rough volatility |

| published on 2022-04-25 [q-fin.CP] 🔗 Elisa Alòs, Fabio Antonelli, Alessandro Ramponi, Sergio Scarlatti CVA in fractional and rough volatility models |

Label #13, 24 articles, keywords: Volatility Models, Modeling Volatility, Models Volatility, Volatility Model, Volatility Pricing

| published on 2023-09-17 [stat.AP, math.PR] 🔗 Giacomo Ascione, Michele Bufalo, Giuseppe Orlando Modeling Volatility of Disaster-Affected Populations: A Non-Homogeneous Geometric-Skew Brownian Motion Approach |

| published on 2023-09-05 [econ.EM, cs.AI, q-fin.CP] 🔗 Chen Liu, Minh-Ngoc Tran, Chao Wang, Richard Gerlach, Robert Kohn DeepVol: A Pre-Trained Universal Asset Volatility Model |

| published on 2023-08-28 [q-fin.MF, q-fin.CP] 🔗 Benjamin Joseph, Gregoire Loeper, Jan Obloj Joint Calibration of Local Volatility Models with Stochastic Interest Rates using Semimartingale Optimal Transport |

| published on 2023-05-18 [q-fin.MF, math.PR, 91G20, 60H10, 60J65, 91G80] 🔗 Alexander Gairat, Vadim Shcherbakov Extreme ATM skew in a local volatility model with discontinuity: joint density approach |

| published on 2023-04-29 [q-fin.MF, math.OC] 🔗 Gregoire Loeper, Jan Obloj, Benjamin Joseph Calibration of Local Volatility Models with Stochastic Interest Rates using Optimal Transport |

Label #14, 13 articles, keywords: Stochastic Volatility, Markets Volatility, Volatility Exuberance, Volatility Statistical, Of Volatility

| published on 2023-09-01 [q-fin.CP, cs.NA, math.NA] 🔗 Fabien Le Floc'h Instabilities of Super-Time-Stepping Methods on the Heston Stochastic Volatility Model |

| published on 2023-02-14 [q-fin.MF, 91G10, 93E20, 60G15] 🔗 Minglian Lin, Indranil SenGupta Analysis of optimal portfolios on finite and small-time horizons for a multi-dimensional correlated stochastic volatility model |

| published on 2022-11-23 [q-fin.PR] 🔗 Zheng Gong, Wojciech Frys, Renzo Tiranti, Carmine Ventre, John O'Hara, Yingbo Bai A new encoding of implied volatility surfaces for their synthetic generation |

| published on 2022-03-24 [q-fin.ST, math.PR, math.ST, stat.TH] 🔗 Rama Cont, Purba Das Rough volatility: fact or artefact? |

| published on 2021-11-10 [q-fin.ST] 🔗 Noriyuki Kunimoto, Kazuhiko Kakamu Is Bitcoin really a currency? A viewpoint of a stochastic volatility model |

Label #15, 11 articles, keywords: Volatility Models, Stochastic Volatility, Volatility Evolution, Volatility Investor, Rough Volatility

| published on 2023-05-20 [econ.GN, q-fin.EC] 🔗 Giampiero M. Gallo, Demetrio Lacava, Edoardo Otranto Volatility jumps and the classification of monetary policy announcements |

| published on 2023-05-01 [q-fin.PR, math.PR, 60G22, 35K10, 65C20, 68T07, 91G60] 🔗 Antoine Jacquier, Zan Zuric Random neural networks for rough volatility |

| published on 2022-11-23 [q-fin.CP] 🔗 Amin Izadyar, Shiva Zamani Investor base and idiosyncratic volatility of cryptocurrencies |

| published on 2022-07-04 [q-fin.CP, cs.AI, q-fin.ST, stat.ML, 91-10, I.5.m] 🔗 Di Zhang, Qiang Niu, Youzhou Zhou Modeling Randomly Walking Volatility with Chained Gamma Distributions |

| published on 2022-01-10 [q-fin.ST, q-fin.CP] 🔗 Mei-Ling Cai, Zhang-HangJian Chen, Sai-Ping Li, Xiong Xiong, Wei Zhang, Ming-Yuan Yang, Fei Ren New volatility evolution model after extreme events |

Label #16, 28 articles, keywords: Volatility Prediction, Volatility Forecasting, Volatility Models, Volatility Clustering, Stochastic Volatility

| published on 2023-10-28 [q-fin.ST] 🔗 Jiaer He, Roberto Rivera A Modeling Approach of Return and Volatility of Structured Investment Products with Caps and Floors |

| published on 2023-02-14 [econ.EM] 🔗 Giorgio Calzolari, Roxana Halbleib, Christian Mücher Sequential Estimation of Multivariate Factor Stochastic Volatility Models |

| published on 2023-01-24 [q-fin.MF, q-fin.ST] 🔗 Kenichiro Shiraya, Tomohisa Yamakami Constructing Copulas Using Corrected Hermite Polynomial Expansion for Estimating Cross Foreign Exchange Volatility |

| published on 2022-11-27 [q-fin.MF, stat.CO, 62P05, 91G60, G.3] 🔗 Jarosław Gruszka, Janusz Szwabiński Parameter Estimation of the Heston Volatility Model with Jumps in the Asset Prices |

| published on 2022-10-05 [q-fin.CP, cs.LG] 🔗 Ananda Chatterjee, Hrisav Bhowmick, Jaydip Sen Stock Volatility Prediction using Time Series and Deep Learning Approach |